.svg)

Go Back

Top 5 Nigerian Bank Cards You Need to Navigate International Payments

By

Ibukun

February 10, 2026

5

mins read

Over the past few years, foreign exchange scarcity and FX reserve management measures forced many Nigerian banks to suspend or severely limit international payments on naira debit cards. As a result, Nigerians had to look for alternative ways to pay for foreign subscriptions, online purchases, and international services.

These alternatives included opening domiciliary accounts, creating multiple virtual dollar cards, holding cash in foreign currencies, or relying on virtual wallets to complete international transactions.

While these options worked, they often came at a higher cost. Many international platforms priced their services using dollar-based exchange rates, even when prices appeared in naira. In practice, this meant Nigerians paid the dollar equivalent, and often more, for services that were technically available in naira.

In 2026, however, some Nigerian banks have re-enabled naira debit cards for international payments, both online and abroad. This has reopened access to foreign spending, though usually within clearly defined limits. Which Nigerian bank cards work best for international payments today, and what should you know before using them?

Opay

The Opay card has become a favourite among Nigerians who shop frequently on international e-commerce platforms such as Shein, Temu, and AliExpress. Because these platforms already display prices in naira, Opay users can pay directly without incurring additional currency conversion fees.

Opay has also integrated directly with some of these platforms, allowing users to make payments without linking their card details or sharing sensitive information. This extra layer of security makes the Opay card particularly attractive for online shopping and low-friction payments.

Providus Bank

Providus Bank has become a reliable option for Nigerians struggling to pay for Apple services and other foreign subscriptions. Its Naira debit card can be added directly to an Apple ID, enabling seamless payments for services such as Apple Music and iCloud.

One of Providus Bank’s biggest advantages is its relatively high international spending limit. Customers can spend up to $3,000 per month on international transactions using the bank’s naira debit card, placing it among the most flexible options currently available.

GTBank

GTBank allows customers to use their naira debit cards for international payments, both online and while travelling, but within defined limits.

International spending, including online purchases, foreign subscriptions, and POS payments abroad, is capped at $1,000 per quarter. In addition, cash withdrawals from ATMs outside Nigeria are limited to $500 per quarter. These limits make the GTBank card useful for short trips or light foreign spending, but less ideal for extended travel.

FirstBank

FirstBank has more restrictive international spending limits than many other Nigerian banks. On standard FirstBank naira debit cards, international transactions are generally capped at around $500 per month.

The FirstBank Naira MasterCard is even more limited, allowing only $100 per month for international spending. Overseas ATM withdrawals on the card are also capped at $100 per day, which can significantly limit access to cash while travelling.

Wema Bank

Wema Bank’s naira debit cards — including ALAT Visa and Mastercard options — have been re-enabled for international payments. These cards typically come with a monthly international spending limit of around $500.

They can be used for online purchases, POS payments abroad, and ATM withdrawals, making them a functional mid-range option for Nigerians who need occasional access to foreign payments.

What to know before using Nigerian bank Cards abroad

International spending limits vary widely across Nigerian banks. Some cards operate on monthly caps, while others use quarterly limits, so it’s important to confirm both the amount and the reset period.

Most banks also require users to manually enable international transactions in their mobile apps or online banking platforms before payments can be processed.

Fees and exchange rates still apply to all international transactions. Payments are processed in the foreign currency at the prevailing exchange rate, which may differ from the rate displayed at checkout.

Higher-tier or premium debit cards generally offer better terms, including higher limits and more consistent acceptance than basic naira cards.

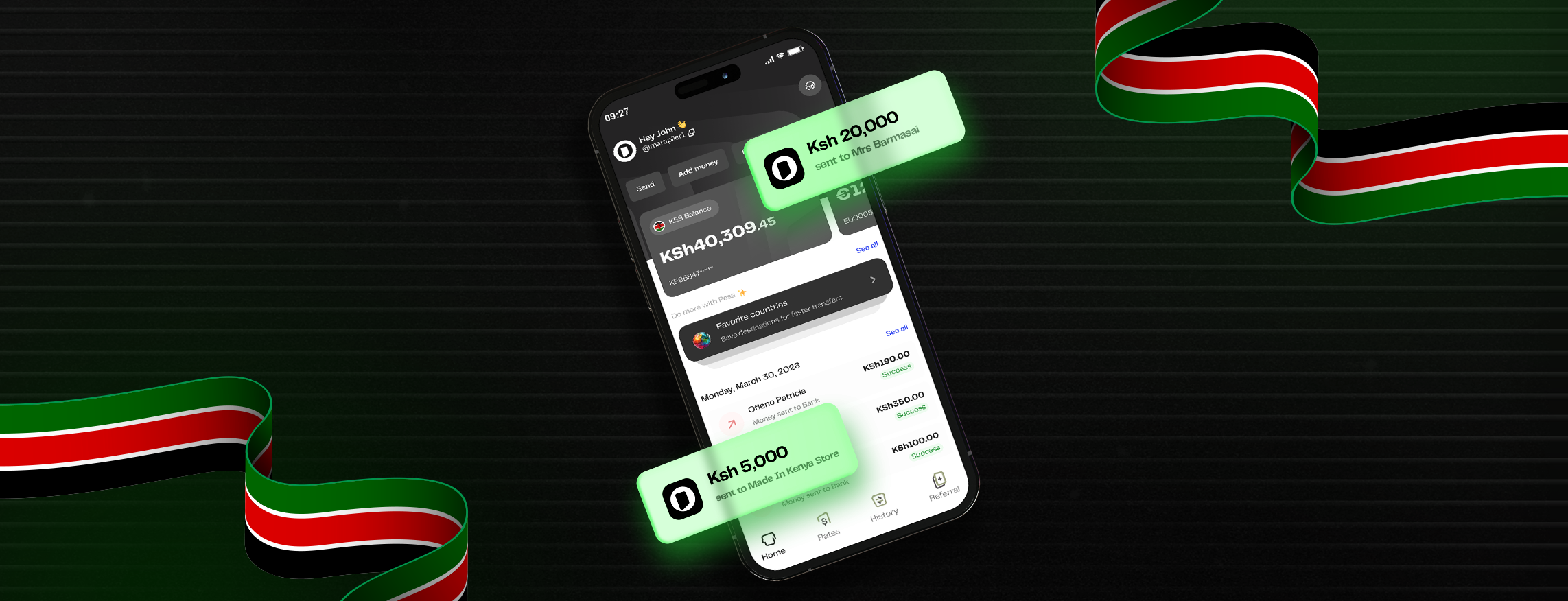

Why you should have your Pesa wallet on standby

While Nigerian bank cards are once again useful for international payments, their limitations become more obvious during holidays, extended travel, or frequent foreign spending. Monthly caps, reduced ATM withdrawal limits, and inconsistent acceptance mean users often have to plan spending around card restrictions rather than actual needs.

This is why many Nigerians now combine local bank cards with multi-currency payment options. Having access to foreign-currency wallets allows travellers to pay for flights, accommodation, subscriptions, and everyday expenses abroad without interruptions or constant limit checks.

For international travel and payments, Nigerian bank cards might seem reliable, but having a Pesa wallet on standby gives you flexibility when card limits get in the way.

Related articles

See all

Think money

Think Pesa

From home to abroad, and everywhere in between. We’ll help you send, receive, and convert your money with ease.

Download the appDownload the app

Join thousands of users sending money

Scan the QR code below with your phone

and you’ll get a link to get started