.svg)

Go Back

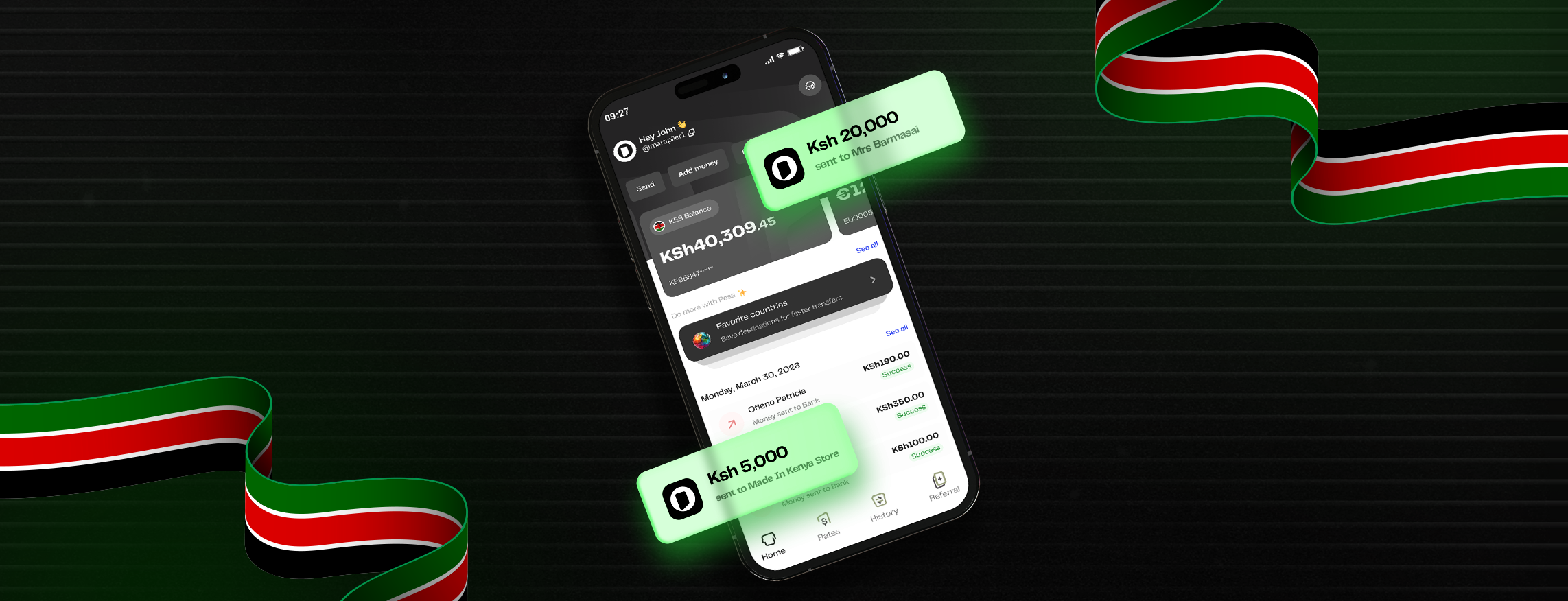

The Immigrant’s Guide to Managing Money Stress-Free Across Borders

By

Ibukun

February 4, 2026

5

mins read

Moving to another country is hardly an easy process, and managing finances as an immigrant is one of the most underestimated challenges. Between multiple currencies, international transfers, family obligations, and unfamiliar financial systems, even the most financially literate can feel overwhelmed by the process.

Fortunately, for most, navigating your finances can be much less tedious when structured properly. This guide walks through practical, realistic steps immigrants can take to reduce friction, avoid unnecessary costs, and regain financial clarity.

1. Understand your new financial system

Before deciding on the bank account to open, downloading an app, opening accounts, or moving money around, it’s important to understand what your financial life actually looks like across borders.

Getting clear on your financial reality helps you stop reacting emotionally to money decisions and start making deliberate ones.

Most immigrants are managing at least two financial lives at once:

- Earning income in one country

- Having expenses, savings, or dependents in another

This often means:

- Earning in one currency and spending in another

- Supporting family back home

- Paying international fees without realising it

Start by mapping:

- Where your money comes from

- Where it goes

- Which currencies you actually need

2. Separate your money (based on your needs)

This is a hack, even for non-immigrants. One of the biggest drivers of money stress is mixing funds meant for different purposes. When everything sits in one place, it becomes difficult to tell what is safe to spend, what should be saved, and what already has obligations attached.

Instead, organise funds by purpose:

- Daily expenses

- Savings

- International obligations

- Business or freelance income

Using structured accounts or a multi-currency wallet helps you:

- Avoid accidental overspending

- See your real financial position clearly

- Reduce emotional decision-making

3. Use multi-currency accounts to reduce conversion losses

Frequent currency conversions are among the most common and least visible ways immigrants lose money. Small FX differences and repeated fees add up quickly, especially for people who earn or send money internationally.

Multi-currency accounts allow you to hold, receive, and manage different currencies without converting immediately.

This allows you to:

- Hold multiple currencies at once

- Receive money in foreign currencies

- Convert only when rates are favourable

This is particularly useful if you:

- Earn internationally

- Send money home regularly

- Pay overseas suppliers or tuition fees

4. Plan your international transfers

International transfers often become stressful because they are treated as emergencies. Rushed transfers usually come with higher fees, poorer exchange rates, and less transparency.

Planning transfers in advance gives you more control over timing, costs, and outcomes.

To reduce stress:

- Schedule regular transfers instead of ad-hoc ones

- Understand transfer fees and exchange rates upfront

- Avoid platforms that hide charges in poor FX rates

Look for transparent services that clearly show:

- Fees

- Delivery timelines

- Exchange rates

5. Build your emergency savings fund in the right currency for you

Emergency funds are only helpful if they are accessible when you need them. For immigrants, this often means thinking beyond a single location or currency, since your emergency savings might not be for you alone but for dependents as well.

Holding all emergency savings in one country can lead to panic transfers and poor financial decisions during urgent situations.

A practical approach is to:

- Keep emergency funds accessible

- Hold them in the currency or currencies you are most likely to need quickly

For many immigrants, this means:

- Part of their emergency savings is saved where they reside

- Part is saved in their home country

6. Support your family within reason

Supporting family across borders is common and meaningful, but it can also become financially draining when handled informally or emotionally.

Creating structure around family support protects your finances and helps maintain healthy boundaries.

To manage this sustainably:

- Agree on fixed amounts or schedules

- Avoid impulse transfers driven by guilt

- Separate “support money” from personal savings

7. Track everything

You don’t need complex spreadsheets or advanced budgeting tools to stay in control of your finances. What matters most is visibility.

Tracking your money helps you understand patterns, identify leaks, and plan future transfers more confidently.

At a minimum, keep track of:

- Monthly inflows and outflows

- Transfer costs

- Savings progress

8. Choose the right tools for cross-border living

Many financial platforms are designed for people who live and earn in one country. Immigrants often need tools that acknowledge cross-border realities.

Using platforms built for international use reduces friction and decision fatigue.

When choosing tools, prioritise:

- Multi-currency support (Like Pesa)

- Transparent international transfers

- Flexibility for personal and business use

- Regulated partners and compliance standards

9. Don’t ignore compliance and documentation

For immigrants running businesses or freelancing internationally, compliance is an important part of financial stability.

Keeping proper records helps prevent issues with banks, partners, and regulators.

Make sure to:

- keep transaction records

- understand basic local regulations

- maintain required compliance documentation

Build a system that works for you!

Managing money stress-free across borders isn’t about perfection or constant optimisation. It’s about creating systems that work even when life gets busy or unpredictable.

When your money has structure, confidence follows.

Financial stability comes from:

- systems over emotion

- planning over panic

- clarity over complexity

Related articles

See all

Think money

Think Pesa

From home to abroad, and everywhere in between. We’ll help you send, receive, and convert your money with ease.

Download the appDownload the app

Join thousands of users sending money

Scan the QR code below with your phone

and you’ll get a link to get started