.svg)

The United Kingdom is one of the world’s leading remittance-sending countries because of its large international population and strong financial system. Every year, billions of pounds leave the UK through remittances as migrants send money to support their businesses, communities, and households that depend on the funds sent for education, healthcare, food, housing, and investments.

These transfers play a major role in the global economy and are especially important for developing countries that rely heavily on money sent from overseas workers. In recent years, digital payment platforms, mobile apps, and fintech companies have changed how people transfer money internationally. Transfer costs have fallen, digital remittances have grown rapidly, and more people now prefer mobile-based transfers instead of traditional cash services.

This statistical report spotlights the UK remittance in detail, including market size, sender demographics, top destination countries, transfer costs, industry trends, digital adoption, and future forecasts. The figures and insights are based on data from the Migration Observatory at the University of Oxford, Statista, Pesa, Remitly, and market research reports.

Top UK Remittance Statistics

- The UK digital remittance market is forecast to grow at a 16.7% compound annual growth rate (CAGR) between 2025 and 2030

- By 2028, the market is expected to surpass $12.5 billion

- As of late 2025, non-bank providers control over 85% of the UK outbound remittance market by volume

- Nigeria & Ghana receive the lion's share of UK-to-Africa flows. In 2024, remittances to Nigeria accounted for nearly 1% of Nigeria's total GDP

- The UK digital remittance market generated approximately $1.53 billion in revenue in 2024

- According to estimates from the Migration Observatory, migrants in the UK sent approximately £9.3 billion abroad in 2023

- The market is currently expanding at a CAGR (Compound Annual Growth Rate) of 2.2%

Overview and Market Size of the UK Remittance

The UK’s position is unique due to its historical ties with Commonwealth nations. This creates thick remittance corridors, high-volume routes between the UK and countries like India, Pakistan, Nigeria, and Ghana, which allow for more competitive pricing and a wider variety of service providers than in many other European nations.

As of 2026, the UK remittance market continues to grow. While the global economy has faced inflationary pressures, the UK’s migrant population's commitment to supporting families abroad remains unwavering.

- Projected Value: By 2028, the market is expected to surpass $12.5 billion.

- Total Annual Outflow: Current estimates place formal remittance outflows from the UK at approximately $11.46 billion (£9.1 billion)

- Market Growth: The market is currently expanding at a CAGR (Compound Annual Growth Rate) of 2.2%.

- The UK is one of the largest remittance-sending countries in Europe. According to estimates from the Migration Observatory, migrants in the UK sent approximately £9.3 billion abroad in 2023. This represented a recovery after the pandemic slowdown, although inflation-adjusted remittance levels remained below pre-pandemic figures.

- The UK also receives inward remittances. In 2023, the country received around £3.6 billion from overseas senders. However, outward remittances remain significantly higher than inward flows.

- Remittances from the UK accounted for approximately 0.34% of the country’s GDP in 2023. While this may appear small, it still places the UK among the major global remittance source countries.

- As of late 2025, non-bank providers control over 85% of the UK outbound remittance market by volume.

UK Remittance Demographics

Remittance senders in the UK are mostly migrants supporting family members in their home countries. According to household survey data cited by the Migration Observatory:

- Around 27% of foreign-born residents in the UK sent remittances in 2021/2022.

- Approximately 32% of non-EU migrants sent money abroad.

- Only 13% of EU migrants reported sending remittances.

- About 8% of UK-born residents also sent money overseas.

The UK sends remittances to countries all around the world, but certain corridors dominate because of large diaspora populations. According to the Migration Observatory briefing:

- 91% of remittance senders said they transferred money to support friends or family.

- 11% supported community projects.

- 3% used remittances for investments.

- 3% sent money to repay loans.

Migrants from Africa and the Middle East were among the most likely to regularly send money home. The average amount sent annually varies widely by income and nationality, but some studies estimate yearly remittances range from £1,000 to between £1,000 and £3,500 per sender.

According to World Bank estimates referenced by the Migration Observatory, the top remittance destinations from the UK include:

- India

- Pakistan

- Nigeria

- Bangladesh

- Ghana

- Jamaica

- Somalia

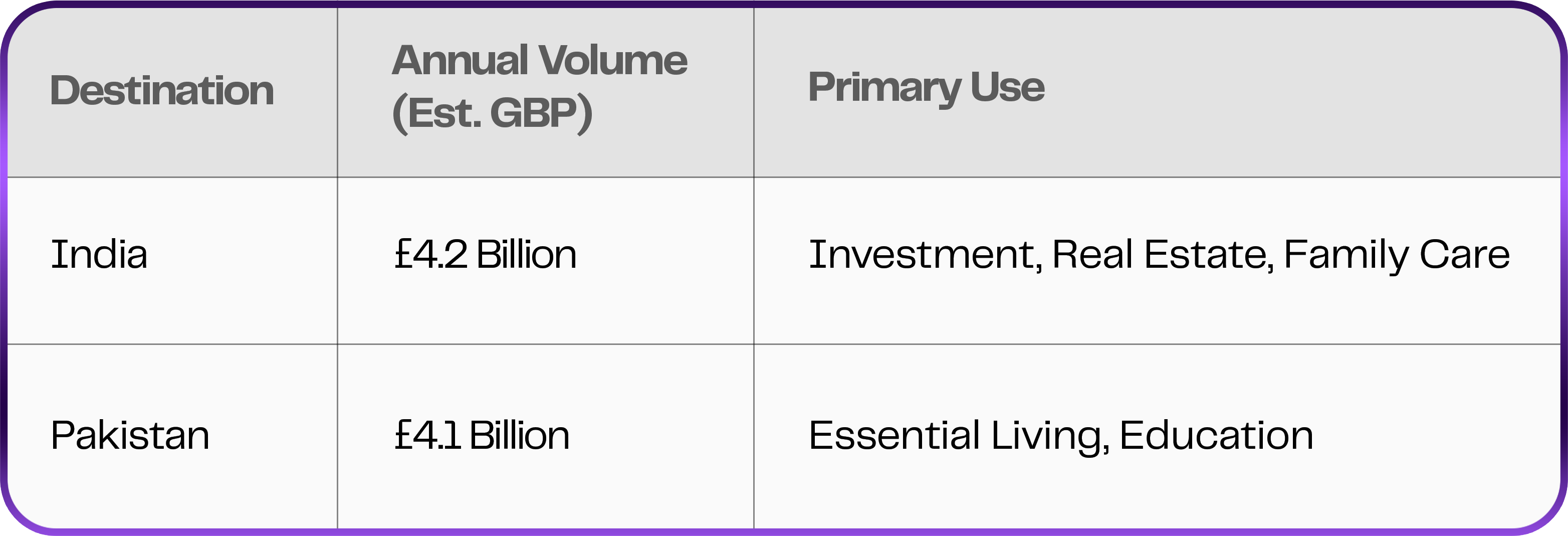

India consistently ranks among the largest recipients of UK remittances, thanks to the large Indian diaspora living in Britain.

Key trends include strong use of digital transfers, low transaction fees, and high frequency of family support payments. India is also one of the cheapest destinations for sending money from the UK, with transfer costs below the UN target of 3%.

Pakistan is another major remittance destination. According to recent estimates, Pakistan and India together account for billions of pounds in transfers annually. Bank transfers to Pakistan are among the cheapest remittance corridors from the UK, with some services charging fees of less than 1%.

Nigeria is one of Africa’s largest recipients of remittances from the UK, due to the large Nigerian community living in Britain.

Remittances to Nigeria are commonly used for school fees, healthcare, family upkeep, business investments, and housing development. Digital remittance apps are becoming increasingly popular for UK-to-Nigeria transfers due to their speed and convenience.

Some smaller economies depend heavily on remittances from the UK relative to their GDP. These include Bermuda, Somalia, Jamaica and The Gambia.

Top Destinations of the UK Remittance

The UK’s reach is truly global, but the concentration of funds in a few key regions is striking.

The following table illustrates the estimated annual outflows to the UK's primary remittance partners:

The UK is perhaps the most important European source of funds for the African continent.

- Nigeria & Ghana receive the lion's share of UK-to-Africa flows. In 2024, remittances to Nigeria accounted for nearly 1% of Nigeria's total GDP.

- Unfortunately, Africa remains the most expensive continent to send money to. The average cost to send £200 to a Sub-Saharan African country from the UK is roughly 8.1%, significantly higher than the 5.2% average for South Asia.

UK Remittance Transfer Costs and Fees

The United Nations Sustainable Development Goal (SDG) 10.c aims to reduce the transaction costs of migrant remittances to less than 3% by 2030. The UK is closer to this goal than many G7 peers, but there is still work to be done.

- Average UK Cost: 5.8% for a £150 (approx. $200) transfer.

- High-street banks remain the dinosaurs of the industry. The cost of sending money via a traditional UK bank can reach as high as 10% to 12% once you factor in the exchange rate markup (the difference between the mid-market rate and the rate the bank gives you).

Digital-only Money Transfer Operators (MTOs) like Wise, Remitly, and WorldRemit have revolutionised the cost structure.

- Digital-only Avg Cost: ~3.5%.

- Traditional MTO (Cash) Avg Cost: ~6.0%.

The transparency of digital apps, which show fees and the exact exchange rate upfront, has forced traditional players to lower their margins to remain competitive.

Mobile Money and Digital Remittance Trends in the UK

According to market research data, the UK digital remittance market generated approximately $1.53 billion in revenue in 2024 and is expected to grow to $3.76 billion by 2030. The market is forecast to grow at a 16.7% compound annual growth rate (CAGR) between 2025 and 2030.

- Direct-to-Wallet: Transfers from a UK banking app directly to a recipient's M-Pesa, MTN, or Airtel wallet have grown by 40% year-on-year.

- Speed of Settlement: 75% of UK-to-India digital transfers are now instant (settled within 60 seconds).

Several factors are driving digital remittance growth:

- Smartphone adoption

- Faster transfers

- Lower fees

- Better exchange rates

- Real-time tracking

- Convenience

Consumers increasingly prefer mobile apps instead of physical agent locations. Some of the major companies operating in the UK remittance market include:

- Wise

- Western Union

- PayPal

- Remitly

- WorldRemit

While 61% of the market is now digital, the Cash-to-Cash model still exists for a reason. Many recipients in rural areas of Pakistan or the Philippines do not have easy access to ATMs or digital infrastructure. Therefore, companies that offer a Hybrid model (Digital send, Cash pickup) still hold significant market share.

Industry and Providers in the UK Remittance

Remittance providers operating in the UK must comply with the Financial Conduct Authority's regulations. The FCA regulates payment institutions and money transfer operators to help protect consumers against fraud, money laundering, and financial crime. This regulatory environment has helped improve trust in digital remittance services.

The major players include

- Wise (formerly TransferWise) and Revolut lead the way in volume. Their focus is on the interbank rate, appealing to tech-savvy migrants and expats.

- Western Union and MoneyGram have successfully pivoted to digital, now offering robust apps that compete with the fintechs while maintaining their massive physical payout networks.

- Companies like Azimo (Europe-focused) or LemFi (Africa-focused) provide tailored services that often beat the big players on specific routes.

As of late 2025, non-bank providers control over 85% of the UK outbound remittance market by volume, as consumers realise the significant savings offered by non-bank providers.

.png)

Growth and Future Trends in the UK Remittance

A new trend emerging in 2026 is green remittances, where UK senders can choose to offset the carbon footprint of their transaction or send funds specifically tagged for climate-resilient agriculture in their home countries.

While still in its early stages for the average consumer, on-chain remittances are growing. Using stablecoins (pegged to the US Dollar or Sterling) allows for near-zero-cost transfers. We expect more UK-regulated firms to adopt blockchain backends to settle transactions faster.

The FCA is increasingly focused on De-risking. This is the practice where banks close the accounts of remittance companies to avoid money laundering risks. This remains the industry's biggest threat, as it can lead to reduced competition and higher prices for consumers.

UK vs Other G7 Countries

The US is the largest sender ($70bn+), but the UK has a higher percentage of digital-native senders. The UK is consistently cheaper for sending money than Germany, France, or Japan. This is largely due to the London Fintech Effect, which has driven innovation and price wars that benefit the consumer.

Compared with other G7 countries, the UK remains an important source of international remittances. However:

- Germany and France remit a larger share of GDP.

- The United States remains the world’s largest remittance source country.

- The UK still ranks among Europe’s leading outbound remittance markets.

The UK’s large migrant workforce and strong financial infrastructure make it a major player in the global remittance ecosystem.

Conclusion

UK remittance statistics show just how important international money transfers are to millions of families worldwide. Every year, billions of pounds are sent from the UK to countries such as India, Pakistan, Nigeria, Ghana, and many others.

The market continues to evolve rapidly as digital platforms replace traditional cash-based systems. Transfer fees are gradually falling, fintech adoption is increasing, and mobile remittance services are becoming the preferred choice for many users. As it continues to attract global talent, remittance flows will only grow in importance.

For businesses and policymakers, these statistics show a market that is resilient, technologically advanced, and deeply integrated into the lives of millions. Whether it's through a mobile app or a high-street kiosk, the UK’s remittance continues to flow, one transaction at a time.

References

https://migrationobservatory.ox.ac.uk/resources/briefings/migrant-remittances-to-and-from-the-uk/

https://migrationobservatory.ox.ac.uk/resources/briefings/migrant-remittances-to-and-from-the-uk/

https://www.marketresearchfuture.com/reports/uk-remittance-market-46509

https://www.remitly.com/gb/en/landing/money-transfer-remittance-statistics

Related articles

See all

Think money

Think Pesa

From home to abroad, and everywhere in between. We’ll help you send, receive, and convert your money with ease.

Download the appDownload the app

Join thousands of users sending money

Scan the QR code below with your phone

and you’ll get a link to get started